Monthly Behavioral Health Billing Audit Checklist

7 min read

Navigating the world of therapy billing can feel like decoding a foreign language. Between deductibles, co pays, superbills, and reimbursement rates, it’s no wonder so many clients and clinicians find themselves overwhelmed. Whether you’re a therapist building your practice or a client s

Cipher Admin

Cipher Billing Team

Navigating the world of therapy billing can feel like decoding a foreign language. Between deductibles, co pays, superbills, and reimbursement rates, it’s no wonder so many clients and clinicians find themselves overwhelmed. Whether you’re a therapist building your practice or a client s

Navigating the world of therapy billing can feel like decoding a foreign language. Between deductibles, co pays, superbills, and reimbursement rates, it’s no wonder so many clients and clinicians find themselves overwhelmed. Whether you’re a therapist building your practice or a client seeking mental health care, understanding out of network vs in network therapy billing is essential to making informed decisions about cost, coverage, and care quality.

At Cipher Billing, we’ve spent years untangling the complexities of behavioral health insurance billing. In this guide, we’ll break down how each plan works, what clients pay, and how therapists can leverage both models to grow sustainable practices.

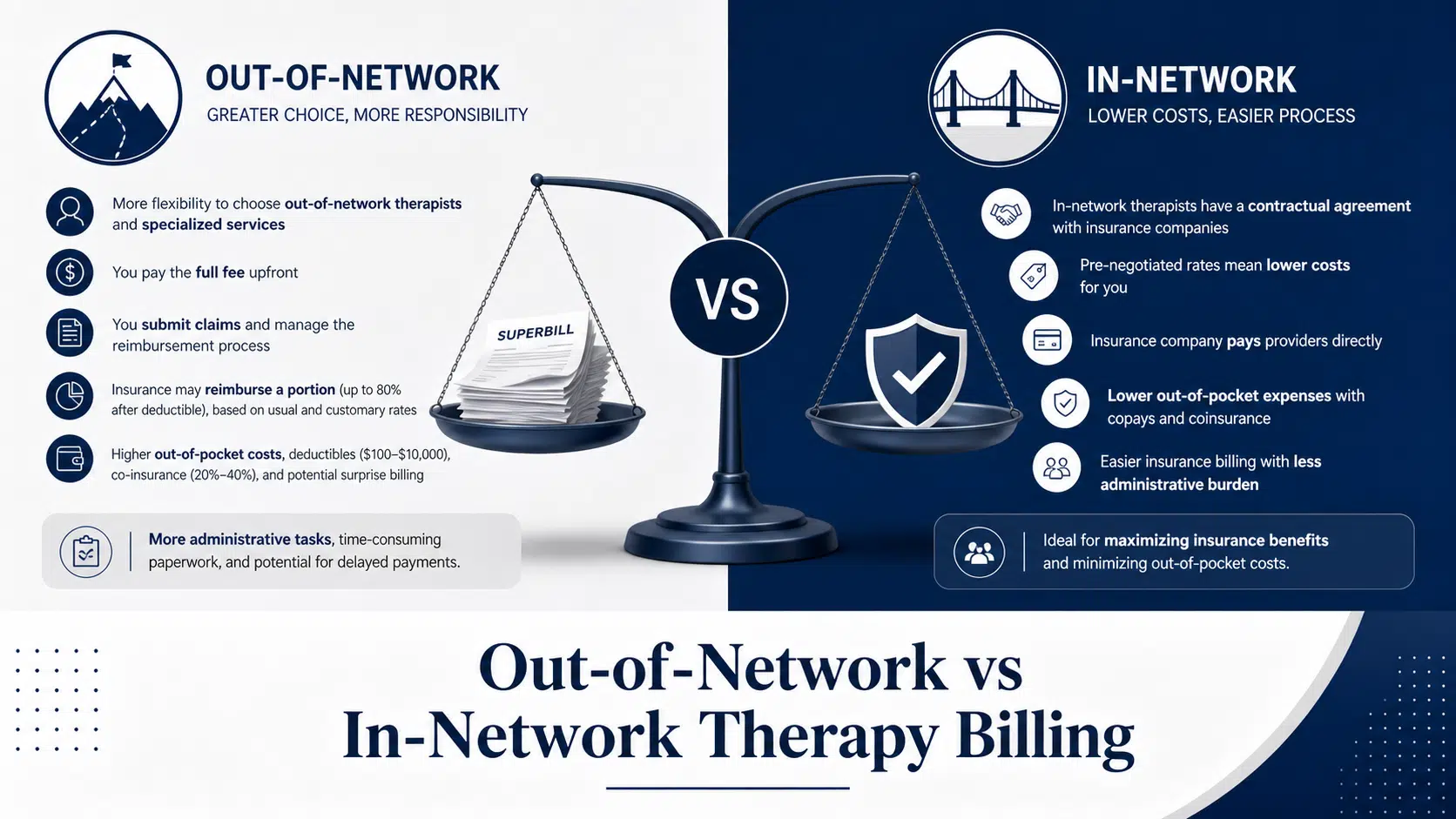

Before diving into the differences, it’s important to understand what “network” means in the context of insurance. An insurance company’s network is a group of healthcare providers who have signed a contractual agreement to offer services at a pre negotiated rate. Providers outside this network operate independently and set their own rates.

In network therapists have signed contracts with an insurance provider to provide services at a discounted rate. This means clients typically pay lower co pays, and the insurance company pays the rest directly to the therapist. In network providers handle most of the insurance billing themselves, reducing the administrative burden on clients.

Out of network therapists don’t have such agreement with the client’s insurance company. They set their own fees, and clients pay the full fee upfront. Afterward, clients can submit claims to their insurance company for potential reimbursement, depending on their out of network benefits.

The primary concern for most clients is cost. Here’s how the two billing models compare:

According to the U.S. Department of Health and Human Services, out of network coverage often involves higher deductibles and co insurance percentages compared to in network services.

With in network therapists, the insurance company pays a pre negotiated portion, and the client covers a small co pay. With out of network therapy, clients pay the full session fee upfront and then seek reimbursement from their insurance provider.

Out of network benefits are features within an insurance policy that allow clients to receive partial reimbursement when seeing therapists outside the insurance company’s network. These benefits vary widely depending on the insurance plan.

Clients with insurance plans that include out of network benefits, such as Preferred Provider Organizations (PPOs) and Point-of-Service (POS) plans, are typically eligible for reimbursement for out of network therapy. HMO plans, on the other hand, rarely offer such reimbursement.

Out of network deductibles can range from $100 to $10,000 per year, and clients must meet this deductible before receiving any reimbursement from their insurance company. After meeting their deductible, clients may be responsible for co insurance, which typically ranges from 20% to 40% of the allowable amount covered by their insurance plan for therapy sessions.

Out of network benefits can allow clients to receive reimbursement for a significant portion of their therapy costs, with some plans covering up to 80% of the session fees, depending on the client’s insurance plan.

This is one of the most common questions clients ask. The honest answer? It depends on your priorities. While in network therapists offer lower costs, out of network therapists often provide more flexibility and specialized services.

The American Psychological Association notes that many therapists prefer to operate out of network to maintain autonomy over treatment decisions and avoid restrictive insurance policies.

When a therapist says they “accept” out of network insurance, it doesn’t mean they bill the insurance company directly. Instead, they provide services and a superbill—a detailed receipt clients can submit to their insurance provider for potential reimbursement.

A superbill includes diagnostic codes, CPT codes, dates of service, and the therapist’s credentials. Clients submit this document to their insurance company along with any required forms to initiate the reimbursement process.

Out of network billing allows therapists to set their own fees and collect them directly from clients, providing greater control over their practice structure and financial arrangements. This model also reduces the time consuming administrative tasks tied to insurance claims and delayed payments from insurers.

Getting insurance reimbursement for out of network services involves a few straightforward steps. Following them carefully can significantly impact how much you recover.

Before scheduling therapy sessions, call the number on your insurance card or review your plan documents to confirm out of network coverage. Ask about your deductible, co insurance percentage, and the allowable amount per session.

You’ll pay the therapist’s full fee at the time of service. This is one of the main differences in network vs out of network billing—clients shoulder the upfront therapy costs.

Submit claims to your insurance company using the superbill provided by your therapist. Some therapists or third-party services will submit claims on your behalf, simplifying the process.

The specific amount reimbursed for out of network therapy depends on individual coverage, with some plans reimbursing up to 80% of the allowable amount after deductibles are met. Reimbursement timelines vary, but most insurance providers process claims within 30 days.

The National Alliance on Mental Illness (NAMI) offers helpful resources for navigating insurance reimbursement and advocating for fair mental health care coverage.

Clients may face varying financial responsibilities depending on whether they choose an in network or out of network provider, with out of network services often resulting in higher out of pocket expenses.

Out of network therapy may result in potential surprise billing when there is a difference between the provider’s charges and what the insurance covers. Always ask about the remaining balance you’ll owe after insurance reimbursement.

The administrative burden is on patients for out of network therapy, as they are responsible for submitting superbills. Out of network therapy typically leads to higher out of pocket costs and requires patients to manage paperwork for reimbursement.

For clinicians, the choice between in network and out of network billing affects everything from cash flow to client volume.

The financial benefits of clear billing practices extend beyond paperwork. Transparent billing builds trust between therapists and clients, ensuring continuity of care and reducing the financial burden that can derail mental health progress.

At Cipher Billing, we specialize in behavioral health insurance billing, helping facilities and private practices maximize insurance reimbursement while minimizing administrative burden. Our team achieves an average of 30.36% out of network reimbursement through aggressive negotiation, far above industry norms.

We also deliver Verification of Benefits (VOB) in just 8–9 minutes, helping clinicians confirm out of network benefits before sessions begin. With a 97% medical necessity appeal success rate, we ensure that denied claims don’t become lost revenue.

So, how do you decide between in network and out of network therapy?

False. Many insurance plans offer robust out of network benefits, especially PPOs. Always check your insurance policy before assuming you’ll pay out of pocket for the entire cost.

Also false. Quality varies across both groups. The decision should be based on fit, specialization, and your insurance coverage—not assumptions about credentials.

Reimbursement depends on your specific insurance plan, deductible status, and the allowable amount. Always verify before committing to a therapist.

The Centers for Medicare & Medicaid Services also provides updated guidance on the No Surprises Act, which protects clients from unexpected out of network costs in certain healthcare services.

As mental health awareness grows, so does the demand for accessible, transparent billing. Both in network and out of network models will continue evolving to meet client needs. Therapists who partner with experienced billing companies like Cipher gain a competitive edge—reducing administrative burden, improving cash flow, and ensuring compliance.

Choosing between in network and out of network therapy isn’t about right or wrong—it’s about what aligns with your goals, finances, and care preferences. Clients benefit from understanding their out of network benefits, while therapists thrive when they choose a billing model that fits their practice vision.

Whether you’re a clinician trying to streamline insurance claims or a client navigating reimbursement, expert support makes all the difference. Cipher Billing exists to bridge the gap between care and compensation—because mental health professionals deserve to focus on what matters most: their clients.

Ready to simplify your behavioral health billing? Visit CipherBilling.com, call (949) 368-0575, or email info@cipherbilling.com. Our team operates Monday–Friday, 8:00 AM – 5:30 PM PST, and is ready to help your practice achieve A Higher Level Partnership.

About the Author

Cipher Billing Team

In This Article

Cipher Billing specializes in behavioral health revenue cycle management. Reach out for a free consultation and see how we can maximize your reimbursements.