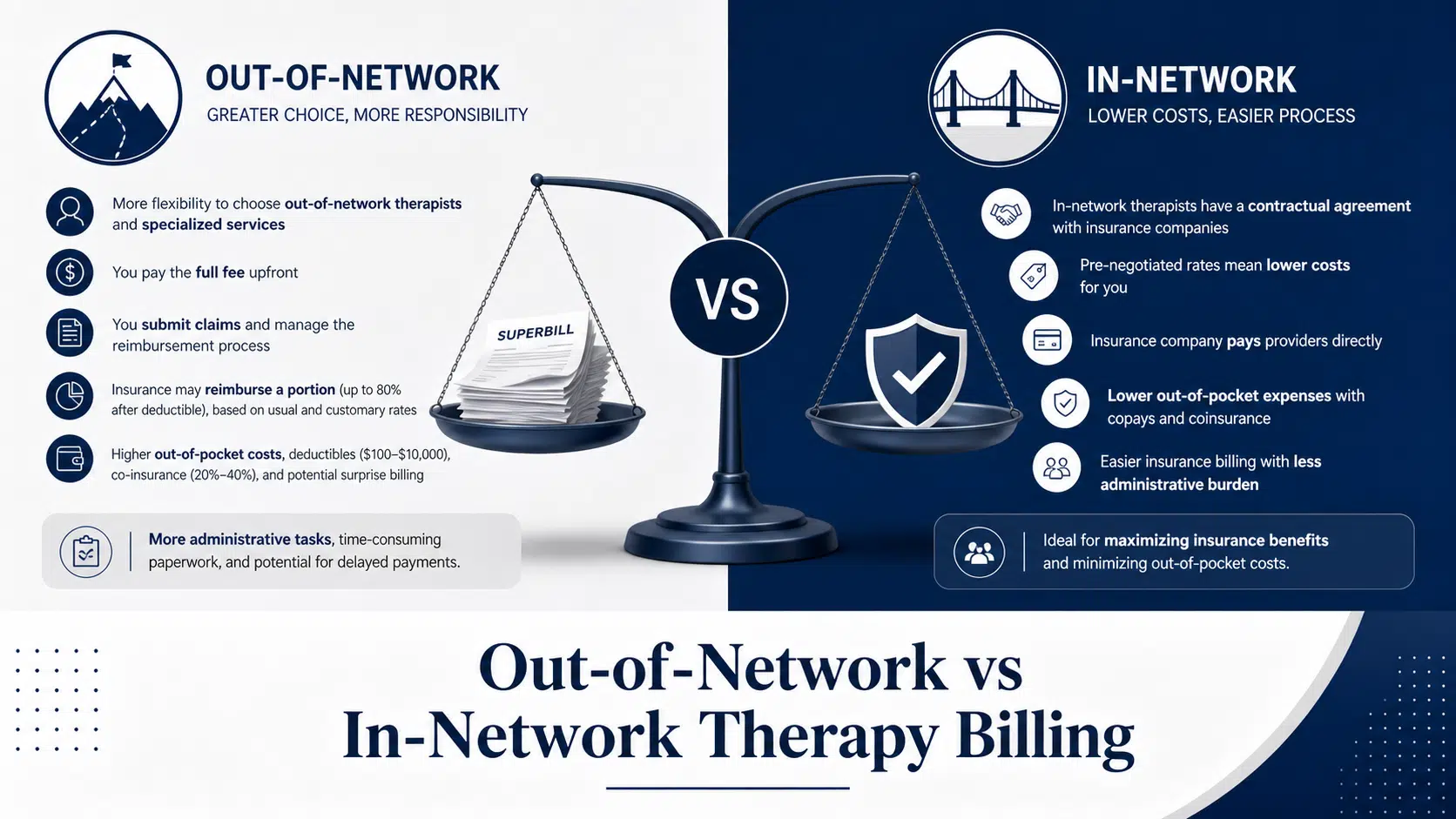

Out-of-Network vs In-Network Therapy Billing

10 min read

Welcome to our comprehensive guide for CipherBilling. The landscape of behavioral health is shifting, and learning about understanding 2026 addiction treatment insurance changes is essential for anyone seeking help. This year brings many updates to how insurance companies handle mental health and su

Cipher Admin

Cipher Billing Team

Welcome to our comprehensive guide for CipherBilling. The landscape of behavioral health is shifting, and learning about understanding 2026 addiction treatment insurance changes is essential for anyone seeking help. This year brings many updates to how insurance companies handle mental health and su

Welcome to our comprehensive guide for CipherBilling. The landscape of behavioral health is shifting, and learning about understanding 2026 addiction treatment insurance changes is essential for anyone seeking help. This year brings many updates to how insurance companies handle mental health and substance use claims. As you plan your healthcare or help a loved one, understanding these complex shifts can save you money and prevent disruptions in care.

For many individuals and their families, the process can feel overwhelming. Dealing with paperwork, deciphering limits, and determining what is paid for can be stressful. However, navigating insurance successfully is possible when you learn the foundational rules and familiarize yourself with your specific benefits.

When we look at previous years, insurance regulations were structured quite differently. Now, the landscape features both new protections and new hurdles for accessing care.

There are major changes at the federal level in how care is managed and how information is shared among providers.

The Affordable Care Act remains a cornerstone of how Americans access mental health treatment and vital recovery resources.

Selecting a marketplace plan correctly ensures that you have proper coverage. Depending on your financial situation, you may even qualify for cost-sharing reductions to lower your overall financial burden.

Mental health parity is a concept meant to guarantee equal treatment for physical and mental health conditions under your insurance policy.

The Addiction Equity Act works alongside parity laws to protect consumers and hold providers accountable.

When assessing your policy, your medical and surgical benefits should match your mental health and substance benefits. Your insurance must not penalize you for seeking care for disorders.

Let’s decode some insurance jargon so you can make informed choices. Understanding terms like deductible, premium, and co pays is incredibly important to maintaining your health and wallet.

Your deductible plays a huge role in your finances and determines when your provider begins contributing to your medical expenses.

Managing your out-of-pocket costs is a critical part of treatment planning. Often, these pocket costs dictate what level of care is feasible.

Every time you visit a doctor, you might pay co-pays. These are fixed amounts you pay for medical services.

The premium tax credit is undergoing significant changes in 2026, leading to higher baseline costs for many enrollees.

Stricter income verification means you must monitor your earnings closely to maintain insurance coverage without facing penalties.

Insurance policies are mandated to assist those with substance use disorders. Treatment for substance abuse and mental illness is critical to community well-being.

If you need residential treatment, you will want robust rehab coverage. Look for plans that comprehensively cover specialized services. A good plan will cover behavioral health services and provide comprehensive addiction treatment coverage.

To access these benefits, you often have to prove medical necessity. Additionally, specific authorizations may be required before you can access particular therapies.

One vital approach to addiction recovery is medication-assisted treatment, paired with proper medication management.

If your insurance denies coverage, you have options and legal protections. Do not give up immediately; there are pathways to challenge these decisions.

Before you begin treatment, speak directly with the facility’s admissions team. The admissions team can help verify your addiction treatment benefits and check your insurance networks.

Be aware that the provider landscape is constantly changing, making it essential to do your research.

Ensure your chosen facility is in network to avoid massive out-of-network bills.

Government-funded health insurance, such as Medicare and Medicaid, is also evolving, affecting the treatments and services available to vulnerable populations.

While Medicaid faces cuts, Medicare has some positive expansions alongside rising premiums.

Departments such as health and human services and the Mental Health Services Administration continuously monitor these shifts. They work to guarantee that individuals receive equitable care compared to other medical care.

To effectively manage these changes, it is important to combat the stigma of seeking help.

Take full advantage of your covered services. Review exactly how your policy handles disorder services and behavioral health services. When the new plan takes effect at the start of the calendar year, be ready to use these essential resources.

During early recovery, you shouldn’t have to worry excessively about money and substance use triggers caused by financial stress. Knowing what happens when coverage begins gives you peace of mind and allows you to focus solely on your medical recovery.

Your recovery journey is paramount. While legislative changes may lead to higher costs for some individuals despite improved parity in addiction-treatment insurance, staying informed keeps you empowered. Remember, mental health treatment and ongoing addiction treatment are critical investments in your future. By understanding these 2026 updates, you can secure the rehab coverage you deserve without risking your financial stability.

About the Author

Cipher Billing Team

In This Article

Cipher Billing specializes in behavioral health revenue cycle management. Reach out for a free consultation and see how we can maximize your reimbursements.